The Rate Shopping System That Saves You $1,500 on Your Mortgage

You're sitting at the kitchen table with two mortgage offers. One has a lower rate but higher fees. The other offers "no points" but something called an origination fee. Your broker says to go with Lender A. Your realtor's friend says Lender B. Your dad says to just use the bank you already have an account with.

You don't know who to trust — because everyone helping you has an incentive that isn't yours. The broker gets paid when the deal closes. The realtor gets paid when you buy. The bank gets paid when you don't shop around.

Freddie Mac research shows that getting just one extra mortgage quote saves an average of $1,500 over the life of the loan. But nearly half of buyers never bother — because comparing offers feels like reading two different languages side by side.

The Mortgage Worksheet is a printable Rate Shopping System — a fill-in-the-blank toolkit you bring to lender meetings that turns confusing offers into a clear, apples-to-apples decision. You'll know exactly what to ask, what to compare, and when to walk away.

Who This Is For

This worksheet is for first-time homebuyers who:

- Have received a Loan Estimate (or are about to) and don't know if the fees listed are standard or inflated

- Are comparing two or more lender offers and can't tell which one actually costs less over time

- Suspect their broker or realtor is steering them toward a preferred lender rather than the cheapest one

- Don't understand "points" — whether to pay them, how to calculate the break-even point, or whether the lender is using them to hide compensation

- Want to walk into a bank branch or broker meeting with a script instead of nodding along and hoping for the best

- Are buying in the US, UK, Canada, Australia, or New Zealand and need region-specific mortgage terminology

What's Inside

The Complete Guide — Full mortgage comparison manual covering the entire lender-shopping process, from pre-qualification to rate lock:

- Side-by-side lender comparison matrix — lenders format offers differently on purpose so you can't compare them directly. This matrix forces every quote into identical columns so the cheapest option jumps out in 15 minutes.

- Points break-even calculator — when a lender says "pay $4,000 upfront to drop your rate," they won't mention it takes 80 months to break even. This one-page worksheet surfaces that math in 60 seconds.

- Junk fee hunter checklist — "processing fee," "admin fee," and "origination fee" can all mean the same thing, and some lenders charge two of them. A line-by-line Loan Estimate audit that flags every doubled-up or inflated charge.

- Rate lock decision tree — locking too early wastes money, locking too late risks a rate hike, and nobody explains the difference. A visual flowchart for the lock-or-float question.

- Negotiation scripts — asking for a "discount" puts you in the weak position. Saying "I have a quote with no origination fee — can you match that?" forces the lender to compete on price, not charm.

- True cost of loan worksheet — the monthly payment number hides the real cost. This worksheet shows total interest, total fees, and total cost over 5, 10, 15, and 30 years so you can compare across your likely ownership horizon.

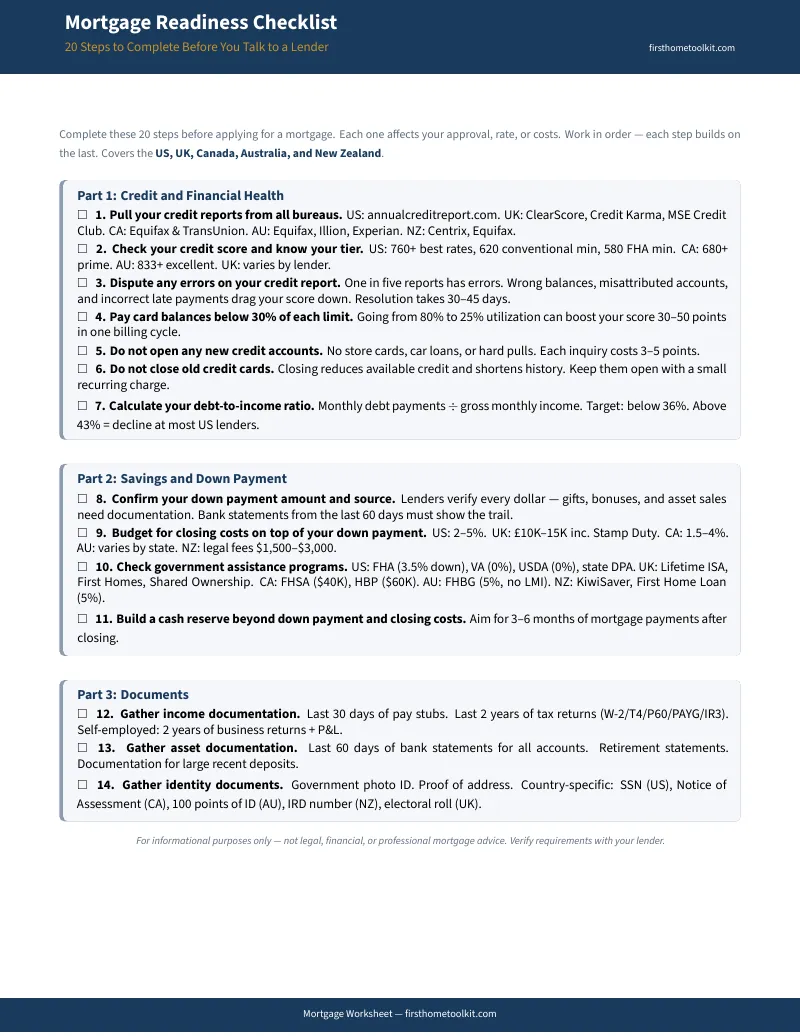

- Pre-approval document organizer — scrambling for a tax return at the last minute signals to lenders you're disorganized, which weakens your position. Every document organized by category, ready before your first meeting.

Standalone Printable Worksheets — Print these separately and bring them to lender meetings:

- Lender Comparison Worksheet — side-by-side grid for up to 4 lender offers (print one per round of quotes). Includes an Excel version with auto-calculating totals.

- Points Break-Even Calculator — fill-in worksheet that tells you in 60 seconds whether paying points saves money

- Junk Fee Checklist — line-by-line Loan Estimate audit with standard vs. challenge classifications

- Negotiation Scripts — word-for-word sentences for rate matching, fee removal, and lender credit requests

- Rate Lock Decision Tree — visual flowchart for the lock-or-float question

- Document Organizer — pre-approval document tracker organized by category

- True Cost Calculator — monthly housing cost worksheet covering P&I, taxes, insurance, PMI, HOA, and maintenance

Region-Specific Worksheets — Mortgages aren't the same everywhere. Dedicated comparison sheets for:

- US — Loan Estimate decoder, APR vs. interest rate, discount points analysis, closing cost breakdown

- UK — Fixed vs. tracker deals, early repayment charges, initial deal period comparison, Stamp Duty reference

- Canada — Stress test impact calculator, 5-year term comparison, CMHC insurance thresholds

- Australia — Offset account vs. redraw comparison, LMI cost calculator, cashback offer analysis

- New Zealand — Table loan vs. revolving credit comparison, cashback vs. rate reduction trade-off

After Using This Worksheet, You'll Be Able To:

- Compare any two mortgage offers in under 15 minutes — even when they use completely different fee structures

- Calculate whether discount points save or cost you money for your specific timeline

- Spot junk fees on your Loan Estimate before you sign anything

- Walk into a lender meeting knowing exactly what to say when you have a competing offer

- Stop relying on your broker's "trust me" and start verifying with math

Why This Instead of a Free Calculator?

Free mortgage tools exist. Here's what they can't do:

- Online calculators (Zillow, Bankrate, NerdWallet) are lead generation engines. You punch in your numbers, they show you a monthly payment, then they show you "recommended lenders" who paid to be on that list. The calculator exists to route you toward specific offers, not to help you compare the ones you already have.

- Government guides (CFPB's Home Loan Toolkit, CMHC, MoneySmart) are comprehensive but 50+ pages of dense prose. They're reference manuals you study at home — not tools you bring to a lender meeting.

- Etsy spreadsheets at $4 are amortization schedules repackaged with aesthetic fonts — the same math available free on any calculator website. They skip the hard parts: points analysis, fee comparison, and negotiation strategy.

- Your broker's advice is valuable — but brokers are paid by lenders when the deal closes. Reddit is full of buyers who felt "steered" toward a preferred lender for the broker's convenience, not the buyer's savings. This worksheet helps you trust and verify.

Free tools are designed to generate leads for lenders. This toolkit serves no master but the buyer — no affiliate links, no "recommended lenders," no one's agenda but yours.

— Less Than a Takeout Dinner. Saves $1,500+.

Freddie Mac research proves that shopping one additional lender saves an average of $1,500 over the life of the loan. Even if this Rate Shopping System only catches one inflated fee or one bad points deal, it pays for itself before you finish filling it out.

A mortgage is the largest financial commitment of your life. You wouldn't take a final exam without studying. This is the cheat sheet.

30-day money-back guarantee. If this worksheet doesn't help you make a more confident mortgage decision, you pay nothing.

Try our free Mortgage Comparison Calculator — compare up to 3 offers side by side, then come back for the full toolkit.

Stop guessing. Print the worksheet. Compare your offers tonight.